Big expenses are part of life — whether it’s renovating your home, buying new appliances, or covering emergency costs.

But when you need extra cash, what’s the smarter move: a personal loan or a credit card?

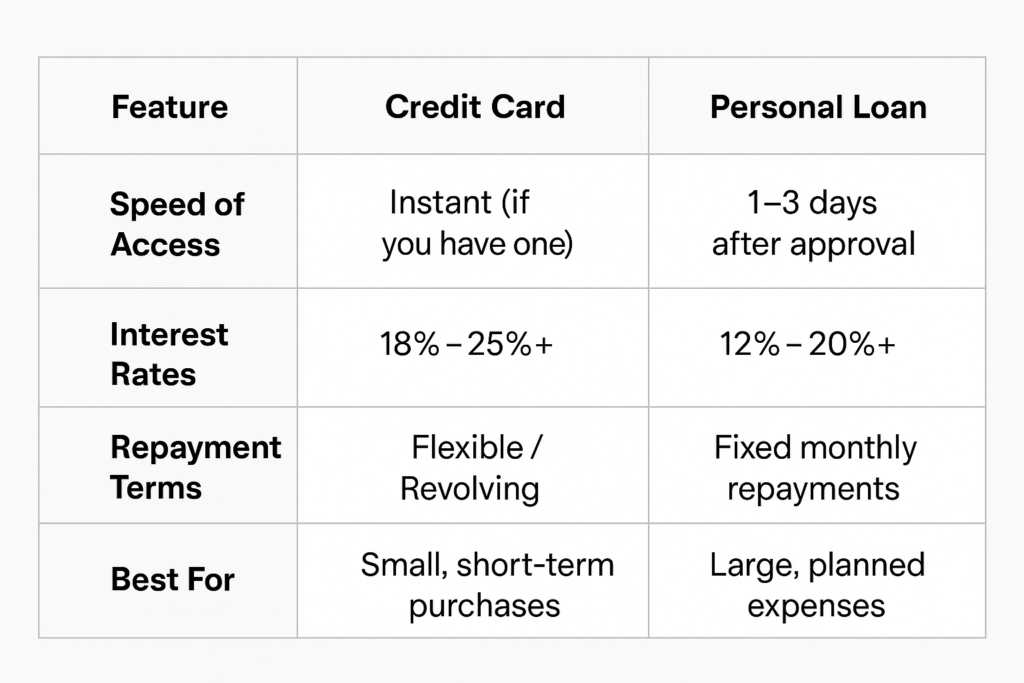

Let’s break it down.

💳 Credit Cards — Fast, Flexible… But Risky if Not Managed

Credit cards are great for smaller expenses or short-term borrowing. You swipe, pay later — simple.

✅ Pros of Using a Credit Card:

- Quick access to funds

- No need to apply for new credit

- Interest-free period (usually up to 55 days)

- Earn rewards (cashback or points)

❌ Cons of Using a Credit Card:

- High interest rates (often 18% – 25%+)

- Easy to overspend

- Minimum payments can trap you in debt

- Lower credit limits

Best For:

- Purchases you can repay quickly

- Smaller once-off buys

- Emergency expenses with quick repayment

💰 Personal Loans — Fixed, Predictable, Lower Interest

Personal loans give you a lump sum upfront — then you repay it monthly over a fixed term.

✅ Pros of Taking a Loan:

- Lower interest rates than credit cards (from 12% depending on your credit)

- Fixed repayment plan — easy to budget

- Larger amounts available

- Good for debt consolidation

❌ Cons of Taking a Loan:

- Takes longer to apply and get approved

- Some upfront fees (initiation/admin fees)

- Penalties for settling early (with some lenders)

Best For:

- Larger purchases over R20,000+

- Home improvements

- Buying appliances, cars, or furniture

- Paying off high-interest debts

So — Which Should You Choose?

If You Can Repay Quickly → Use a Credit Card (and avoid interest)

If You Need Time to Repay → A Personal Loan may be better for lower rates & predictability

😁 Final Tip: Always Compare First

Before applying for any credit — compare offers from multiple lenders.

Rates, fees, and approval times vary — and a quick comparison could save you thousands in interest.

Need a personal loan of up to R150,000? Apply now, one form goes to multiple lenders to get you the best rate!